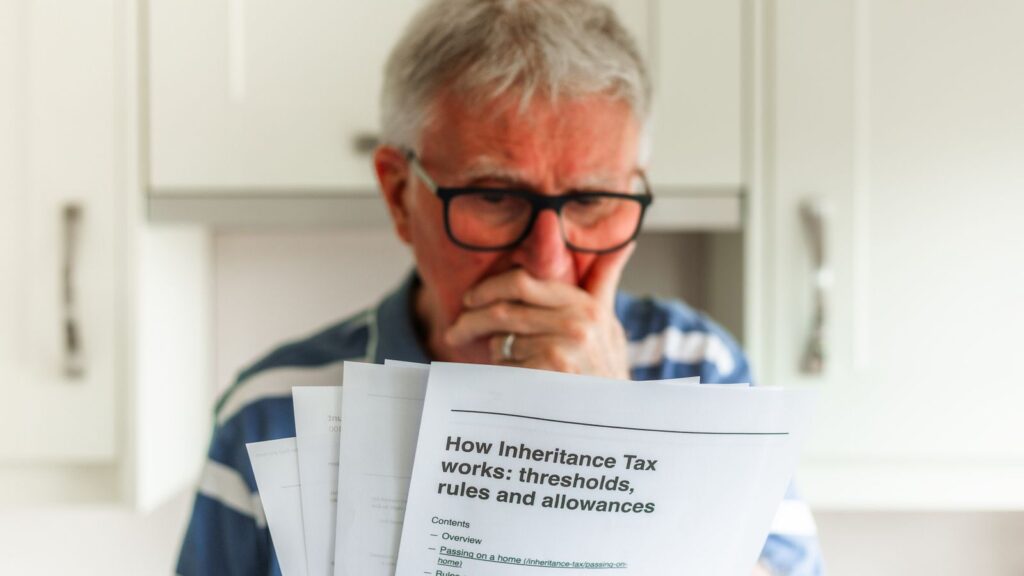

It’s dubbed the “most-hated” tax in the UK, but many of us will need to think about inheritance at some point in our lives.

And from next year, the way it applies to pensions is changing.

Here’s what we know so far about the new rules coming in from April 2027…

Read all our latest tips and money news here

What’s changing?

The government announced that from 6 April 2027, most unused pension funds and pension death benefits will be brought within the value of the estate of someone who has died for inheritance tax purposes.

It marks a major shift from current legislation, which does not consider most pension funds for the tax.

This has seen them increasingly used as a tax-efficient way to transfer wealth rather than for their intended use of funding retirement, according to the government.

HMRC recently released a technical note on the changes, but we’re yet to receive the full details.

Below, we run through the key elements from that note.

Potential admin headache for families

Personal representatives – those appointed to settle the affairs of someone who has died – will be responsible for taking “reasonable steps” to identify the deceased person’s pension savings, work out their value and pay tax on them.

As with other taxable assets, they’ll need to scan through the person’s records and bank accounts, but HMRC says representatives may also need to contact pension companies and insurance schemes themselves to notify them of the death and request information.

The note doesn’t detail what the “reasonable steps” would be in practice.

Irwin Mitchell Solicitors points out that families often face “fragmented records, historic workplace schemes and multiple providers”.

It said in response to the HMRC note: “The manual refers to ‘looking through all the deceased’s papers’, but what about online records, and the passwords needed to access them?”

Income tax rules

Inheritance tax of 40% applies when an estate is valued above a certain threshold when a person dies.

If they pass away after the age of 75, any inherited pension income is usually free of inheritance tax, but withdrawals will be subject to income tax.

However, after the April 2027 changes, the pension amount received by the beneficiary will be liable for inheritance tax first, meaning they will only pay income tax on the remaining amount to avoid a “double tax hit”.

Read more:

Why are there two different state pensions?

The pension trick most people don’t know about

Tax deadline unchanged – but withholding rule introduced

Inheritance tax is due within six months after a donor’s death. If it’s not paid by this time, the amount to be paid will start accruing interest according to the Bank of England’s base rate.

This will be the same for any pension funds liable for the tax, HMRC has confirmed.

But HMRC has introduced a new mechanism where executors can direct pension providers to withhold up to 50% of any lump sum pension benefits that may be subject to inheritance tax for up to 15 months, to make sure pension payments are not made before they’ve settled the tax due.

Personal representatives and beneficiaries can also request that the pension provider pay any tax due directly to HMRC.

Pic: iStock

Exemptions still apply

It will remain the case that if you are married or in a civil partnership, any tax-free allowance you don’t use can be added to your partner’s allowance when they die.

This means a couple can pass on as much as £1m without their estate being subject to inheritance tax.

HMRC has also stated that most “death in service” benefits will remain exempt, but may need to be reported to them by pension scheme administrators.

Joint life annuities and dependents’ scheme pensions are also exempt from the new legislation.

What’s the timeline for changes?

HMRC is working with industry experts to nail down the finer details and exact legislation, with further guidance not expected until later this year or early next year.

Its technical note sets out the following timeline:

- Spring 2026: Publish draft regulations on information sharing requirements

- Spring/summer 2026: Make and lay the regulations on information sharing requirements with a commencement date of 6 April 2027

- Spring/summer/autumn 2026: Continue process design and develop guidance and other support tools

- Autumn/winter 2026/2027: Share draft guidance with industry stakeholders

- Winter/spring 2026/2027: Communications activity to publicise upcoming changes to impacted groups

- Spring 2027: Publish guidance and other supporting materials

Source link

Khamrah by Lattafa for Men - 3.4 oz EDP Spray

4% Off

Ghost Sweetheart Eau de Toilette | Pineapple, Jasmine and Sandalwood | Perfume for Women 50 ml

50% Off

Marc Jacobs Dot Eau De Parfum for Women, 100 ml

42% Off

Ted Baker W Eau de Toilette for Her, Fig Leaf, White Peony and Violet Top Notes, Pink Orchid and Raspberry Middle Notes, 75ml

£11.77 (£15.69 / 100 ml) (as of 09/07/2026 03:55 GMT +01:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Ted Baker Woman Pink Eau de Toilette Spray Floral Green Feminine Fragrance, Opening Notes are Fresh Peach, Bergamot and Tangerine with Warm Musk, Vanilla and Vetiver Base, 100ml

11% Off

Vera Wang Princess Eau de Toilette - 30 ml

Choco Musk 50ml Eau De Parfum for men and women | Chocolate Musk by Jannat Aromas

17% Off

Christina Aguilera Signature Eau de Parfum (50ml) Floral, Fruity & Exotic Scent, Luxury Fragrance for Women

9% Off

Calvin Klein - Eau De Toilette CKIN2U - Calvin Klein Women, Ladies Perfume, Women's Perfume, Calvin Klein Perfume, Calvin Klein One - 150 ml

5% Off

Jimmy Choo Flash Eau de Parfum, 60 ml (Pack of 1)

3% Off

Fruit of the Loom Men's Heavy T Shirt, White, XL UK

28% Off

ATNKE LED Lighted Beanie Cap,USB Rechargeable Running Hat Ultra Bright 4 LED Waterproof Light Winter Warm Gifts for Men and Women/Pink

17% Off

Men's 1/4 Zip Pullover UK Sale Clearance, Fleece Sweatshirt Casual Jumper Long Sleeve T-shirt Top Stand Collar Sweater Plain Pullover Sports Leisure Workwear Quarter Zip Sweater Lightweight Jumpers

£5.88 (as of 12/11/2025 00:52 GMT +01:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Crevice Cleaning Brush, Bathroom Tile Groove Gap Cleaning Brush,Premium Crevice Cleaning Tool Aluminum Support with 15° Angle Magic Brush, Thin Brush for Home Kitchen

19% Off

Wireless Earbuds, Bluetooth 5.3 Headphones in Ear with HiFi Stereo Deep Bass, 4 ENC Noise Cancelling Mic Wireless Earphones 40H Playtime, Bluetooth Earbuds Dual LED Display, IP7 Waterproof, USB-C

42% Off